Targeting Net Zero: Embedding accountability for portfolio decarbonisation that deliver real world outcomes; the Asset Owner and Asset Manager Relationship

A summary and updated version of a chapter originally published in Investment Management, Stewardship and Sustainability (Hart Publishing, 2022). Updated June 2026

Steep reductions in greenhouse gas emissions are needed this decade if the hope of limiting warming to 1.5°C is to remain in sight. That was true when I wrote this chapter in 2022, and it remains the defining challenge for investors today. What has changed, dramatically, is the political and institutional landscape around net-zero commitments, making the question of genuine accountability more pressing than ever.

Over 130 parties to the Paris Agreement have committed to net-zero by mid-century. They are joined by cities, companies, and financial institutions across the globe. But commitment and accountability are not the same thing. The events of 2025 (when several of the Net Zero alliances in the financial sector either collapsed or were materially restructured) serve as a sharp reminder that whilst frameworks matter, the behaviours they embed are more important.

This piece draws on my experience at Brunel Pension Partnership, where I worked from its formation in 2017 until June 2026. It sets out how asset owners can embed genuine accountability for decarbonisation and real world outcomes in their relationships with asset managers, not through declarations, but through selection, appointment, monitoring, and a willingness to act.

Why This Matters for Investors

Climate change presents a systemic and material financial risk to every economy on the planet. Mark Carney’s 2015 Mansion House speech, “Breaking the Tragedy of the Horizon,” crystallised three channels through which this risk flows:

Physical risks arise from the direct impacts of climate-related events: floods, storms, sea level rise damaging assets and disrupting trade.

Liability risks arise when parties suffering loss seek compensation from those responsible, a risk that could hit carbon extractors and their insurers hardest, and may only materialise decades from now.

Transition risks arise from the repricing of assets as policy, technology, and market expectations shift in response to decarbonisation. The speed of this repricing (potentially rapid and disorderly) is the risk most immediately relevant to investment portfolios today.

The Task Force on Climate-related Financial Disclosures (TCFD), which formalised these categories in 2017, remains the standard framework for climate governance and disclosure. Asset owners and managers are increasingly required, not merely encouraged, to evidence how they manage these risks.

The crucial insight is this: genuinely reducing climate risk requires a net-zero economy, not just net-zero portfolios. Shifting carbon exposure between portfolios achieves nothing for the real world. The task is to ensure that investment decisions drive real-economy change in companies’ strategies, operations, and capital allocation.

What Does It Mean to Be a Net-Zero Investor?

The Paris Agreement, designed for national governments, needs translation into practical requirements for investors. The Net Zero Investment Framework (NZIF), developed through the Paris Aligned Investment Initiative (PAII), provides the most comprehensive shared methodology: a common set of actions, metrics, and methodologies through which investors can develop their individual net zero strategies and transition plans.

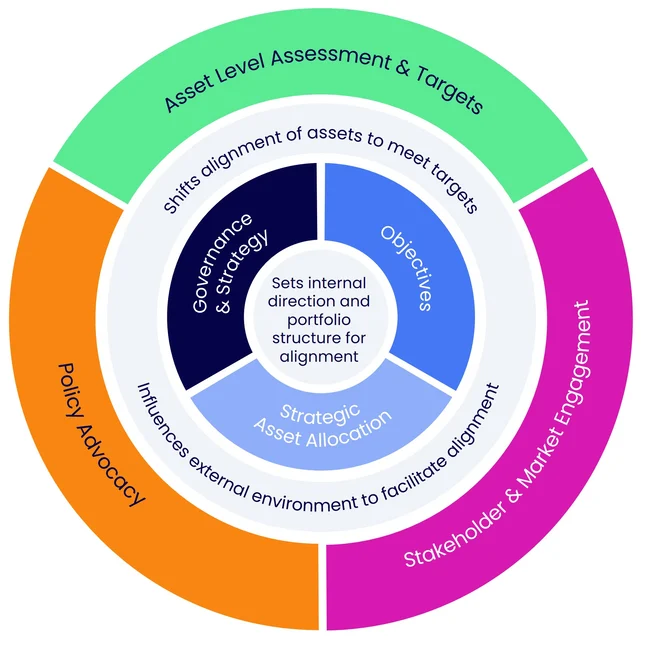

Figure 1: The NZIF Wheel — Net Zero Investment Framework 2.0

The NZIF 2.0 wheel highlights the interconnected nature of each core area and their equal importance. There is no hierarchy: net zero strategies are more likely to be effective when they address the external environment, which itself can either facilitate or inhibit investor activities. The six components are:

Governance and Strategy establishing the basis, legitimacy, and actions required by investors to address climate-related transition risks.

Objectives establishing net zero objectives over a ten-year period, enabling net zero strategy and target performance assessment.

Strategic Asset Allocation integrating net zero objectives into the asset allocation process, complementing traditional risk/return objectives.

Asset Level Assessment and Targets helping investors shift the alignment of underlying holdings to be consistent with net zero goals and objectives.

Stakeholder and Market Engagement facilitating the availability of data, mandates, and investment advice necessary to achieve net zero objectives.

Policy Advocacy addressing barriers to, and capturing opportunities for, net zero alignment created by the wider policy and regulatory environment.

NZIF 2.0, published in June 2024, is an evolution of the original framework informed by three years of implementation experience across more than 200 investors. It emphasises “financing reduced emissions” rather than “reducing financed emissions”, a subtle but important distinction that keeps the focus on real economy outcomes rather than portfolio-level carbon accounting. It now covers six asset classes explicitly, adding Sovereign Bonds, Real Estate, Infrastructure, Private Equity and Private Debt alongside the original Listed Equity and Corporate Fixed Income guidance.

The framework is valuable precisely because it creates shared language and shared expectations across the investment chain. When both asset owner and asset manager are working from the same framework, conversations about portfolio outcomes become far more productive than debates about definitions.

That context makes the events of 2025 more instructive, not less. The Net Zero Asset Managers (NZAM) initiative was relaunched in February 2026 with more than 250 signatories. Brunel led a collective letter to asset managers setting out why signing the NZAM commitment mattered and encouraging them to do so. The rationale was straightforward: if the managers we appointed were publicly committed to the same net-zero objectives, it strengthened alignment across the investment chain and made accountability conversations considerably easier. However, asset owners need to look beyond initiative membership and examine whether underlying behaviours have changed. That is where accountability lives.

Brunel’s Approach: From Policy to Practice

Brunel’s listed markets mandates were outsourced to external asset managers, which alongside allocations to fund managers, general partners and co-investments, meant our leverage over the real economy ran entirely through those relationships: through the selection, appointment, monitoring, and retention of around 200 investment managers across 17 portfolios (albeit with multiple cycles in private markets) built from 2018 onwards.

Our starting point was recognising that the finance system itself was not fit for purpose in dealing with climate change. Our 2020 Climate Policy placed improving the financial system at the centre of our approach. Brunel committed in March 2021 to achieving net-zero by no later than 2050, through the Paris Aligned Asset Owner Commitment. Our Climate Change Policy was updated in 2023 to reflect the NZIF related commitments and by 2025 Brunel had 100% in scope assets (around 92% of AUM) covered by a Net Zero alignment target and monitoring process.

The policy was direct about what this meant for managers:

“We will rigorously, assertively and continuously challenge our investment managers on their analysis and assessment of climate-related risks in their investment practices and processes. We will expect them to continually improve these practices and processes, and will explicitly consider these improvements in our monitoring, management, selection, appointment and reappointment of our investment managers.”

This wasn’t a side commitment. It was built into how every mandate was structured.

Embedding Accountability at Each Stage

Manager Selection: Climate Questions with Real Weight

In Brunel’s tender processes, climate and stewardship questions represented over half the quality and service score in Invitation to Tender documents. Giving questions that weight sends a clear signal: climate policy alignment is not a box-ticking exercise.

What distinguished the strongest responses was honesty. The managers who scored highest were those who clearly described where they faced challenges (for example, the difficulty of conducting climate risk assessments on asset-backed securities due to limited data – see Brunel-Oaktree MAC case study, 2025) rather than presenting a polished but vague commitment to ESG integration.

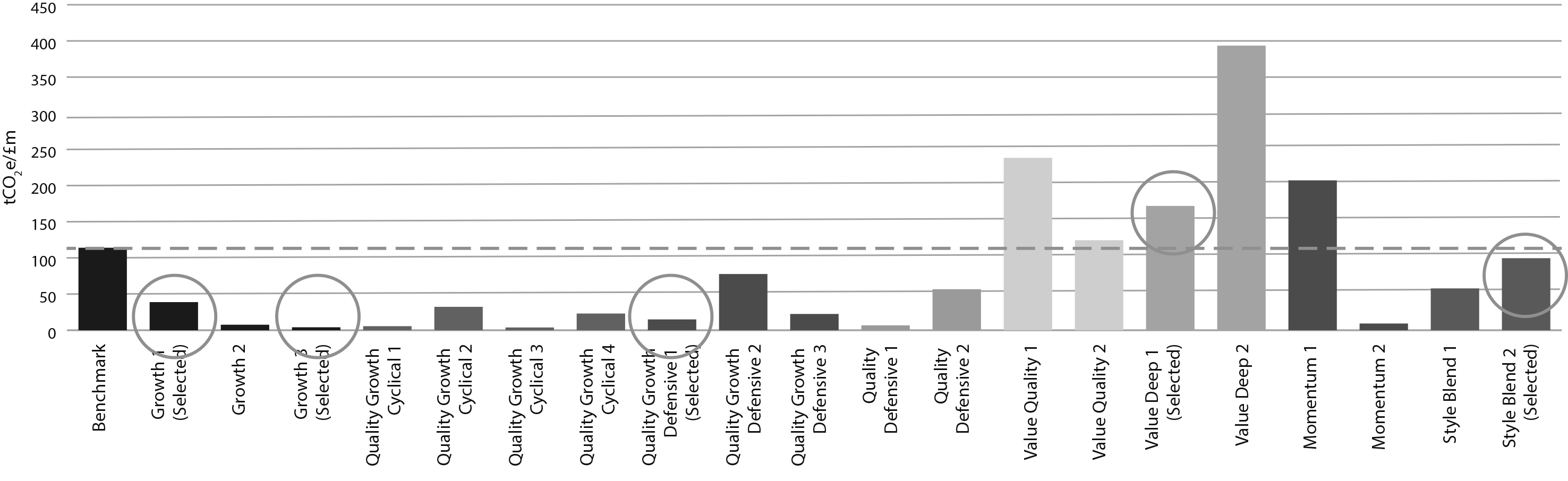

We also used carbon footprinting data as part of due diligence for manager selection. The chart below illustrates how we mapped the carbon intensity of shortlisted managers for a global equity strategy by investment style.

Figure 2: Carbon Intensity of Shortlisted Managers by Style Factor (2019 global equity search)

[Bar chart: weighted average carbon intensity (tCO₂e/£m) by investment style. Selected managers circled. Most below benchmark; Value Manager category notably higher.]

Source: Brunel Pension Partnership

The value category was the outlier, unsurprisingly, since carbon-intensive sectors often have the financial characteristics value managers seek. When analysing one shortlisted value manager, we found 70% of the portfolio’s carbon intensity came from a single holding: LafargeHolcim (now Holcim), one of the world’s largest cement producers.

Rather than treating this as a disqualifier, we discussed it directly with the manager. They demonstrated a clear understanding of Holcim’s climate risks and transition strategy. Using the Transition Pathway Initiative (TPI), an asset-owner-led initiative that assesses companies’ preparedness for the low-carbon transition, we confirmed that while Holcim was not then net-zero aligned, it had a credible long-term strategy. The manager was selected.

This case illustrates a broader point: carbon intensity as a single metric can drive perverse outcomes, pushing managers away from high-emitting sectors that are actively transitioning, rather than toward companies with credible net-zero pathways. The combination of carbon data and forward-looking tools like TPI is far more useful than either alone.

Manager Appointment: The Asset Management Accord

Embedding prescriptive climate requirements (hard-coded emissions-reduction asks) into investment management agreements (IMAs) risks becoming quickly obsolete as methodologies evolve. The industry has seen an increased focus on IMAs that set out outcome-orientated expectations, transparency requirements, and calls for increased public policy advocacy.

Brunel’s earliest attempts to move beyond specific asks led to the development of the Brunel Asset Management Accord, a principles-based document that captures the spirit of the relationship and the expectations on both sides, without requiring every evolution in climate practice to trigger a legal renegotiation.

Three extracts are particularly relevant:

Brunel takes a long-term view of its fiduciary duties and expects the manager to act as if it were a fiduciary investing for the long term.

Brunel expects the managers’ reporting to facilitate its ability to deliver its transparency commitments.

Brunel welcomes open dialogue to explore ways to meet evolving investment needs. The manager will keep Brunel informed of the evolution of its business and investment process so that Brunel can ensure the mandate remains fit for purpose.

The Accord is a two-way commitment. Brunel commits to being long-term and to supporting managers through periods of underperformance. In return, managers commit to evolving their processes, not just to the letter of the mandate, but in pursuit of the outcome it seeks.

Manager Monitoring: Working in Partnership

Over 18 months from January 2020, Brunel worked closely with Invesco to decarbonise the UK Active Equity Portfolio. Invesco’s quantitative approach meant that the solution had to follow the same methodology used to design the portfolio. It sought to integrate carbon data into an existing multi-factor model rather than relying on company engagement to reduce exposure to financed emissions.

The outcome was significant. The carbon intensity of the portfolio fell from 362 tCO₂e/mGBP in March 2019 to 199 tCO₂e/mGBP by December 2020, a 45% reduction, while maintaining the strategy’s factor exposures and expected return profile.

Figure 3: Carbon Intensity of Brunel’s UK Active Equity Portfolio (March 2019 to December 2020)

Date | Portfolio Intensity (tCO₂e/mGBP) | Benchmark |

|---|---|---|

March 2019 | 362 | 316 |

December 2019 | 259 | 282 |

December 2020 | 199 | 278 |

Source: Brunel Pension Partnership / Invesco

This approach was replicated across portfolios. By 2021, all active Brunel portfolios had reduced carbon intensity against 2019 baselines, with the Global High Alpha Portfolio achieving a 50% reduction. This trend has continued, with the table below summarising the closing position of Brunel’s listed market portfolios as at December 2025, as published in the 2026 Climate Change Progress Report.

Carbon Intensity: Brunel Portfolios (2019 to 2025)

Weighted average carbon intensity (tCO₂e/mGBP). Baseline: 31 December 2019. As at December 2025.

Portfolio | 2019 Baseline | 2025 Portfolio | Reduction % |

|---|---|---|---|

Brunel Aggregate Portfolio | 343 | 157 | 54.08% |

Active Portfolios | |||

Global High Alpha Equities | 301 | 160 | 46.97% |

Global Sustainable Equities | 334 | 238 | 28.69% |

UK Active Equities | 282 | 127 | 55.14% |

Emerging Markets Equities | 570 | 163 | 71.34% |

Global Small Cap Equities * | 309 | 150 | 51.50% |

Low Volatility Global Equities | 334 | 107 | 67.96% |

Sterling Corporate Bonds ** | 184 | 96 | 47.91% |

Passive Portfolios | |||

PAB Passive Global Equities | 303 | 117 | 61.46% |

CTB Passive Global Equities | 303 | 140 | 53.89% |

Passive Developed Equities | 303 | 168 | 44.65% |

Passive UK Equities | 281 | 156 | 44.40% |

Passive Smart Beta | 554 | 341 | 38.33% |

* Updated methodology in 2020: December 2020 taken as baseline for Global Small Cap Equities.

** Sterling Corporate Bonds baseline is 31 December 2021.

Source: Brunel Pension Partnership, Climate Change Progress Report 2026.

What the Last Four Years Have Taught Us

The disruption of 2025 was a test of whether net-zero commitments were embedded in practice or simply declared. For asset owners who had genuinely built accountability into their investment processes, through mandate design, tender scoring, monitoring frameworks, and the willingness to terminate, that disruption changed nothing material. For those who had relied on initiative membership as a proxy for progress, it exposed the gap.

My reflections, as in 2022, are that the critical components of genuine asset manager accountability are:

Senior-level commitment and robust governance on your own climate policy: climate must be a strategic risk owned at the top, not delegated to the RI team.

Clear translation from policy to manager expectations, with active monitoring against those expectations, not just at appointment.

Avoiding over-prescription on how outcomes are achieved. Managers know their processes best; they should be accountable for adapting them to meet your objectives.

Welcoming a variety of approaches, which reduces concentration and factor risks in how climate is managed across the portfolio.

Patience and partnership: portfolio-level change typically takes 12 to 18 months to implement well. Relationships that allow honest dialogue about what is and isn’t working are far more effective than adversarial monitoring.

Consistency across your climate policy: what you ask of managers must align with your own engagement, voting, and advocacy positions.

Conclusion

Becoming Paris-aligned remains the challenge of this generation. The political headwinds of recent years, the retreat of some managers from net-zero commitments and the weakening of some coalitions, make the case for embedding accountability in practice, not just in pledges, more urgent, not less.

The finance system was not designed to address climate change. Changing it requires a shift of mindset and a willingness to challenge the conventional wisdom that has shaped investment for generations. That starts with asset owners being explicit, persistent, and honest with themselves and with their managers about what an investor contribution to societal net-zero ambitions requires.

The best progress comes from genuine collaboration. Sharing experiences, including failures, is how the industry learns. The goal, as it always was, is to manage assets in a way that helps beneficiaries prepare not just financially, but for the world they will retire into.

Faith Ward is an independent climate and investment strategist. She was Chief Responsible Investment Officer at Brunel Pension Partnership from 2017 to 2026, where she led the development of Brunel’s climate policy and its implementation through asset manager relationships.

This article draws on a chapter originally published in Investment Management, Stewardship and Sustainability (Hart Publishing, 2022), and is attached below.

References

Brunel Pension Partnership (2026) Climate Change Progress Report 2026.

Institutional Investors Group on Climate Change (IIGCC) (2024) Net Zero Investment Framework 2.0, June 2024.

Task Force on Climate-related Financial Disclosures (TCFD) (2017) Recommendations of the Task Force on Climate-related Financial Disclosures.

Transition Pathway Initiative (2019) Holcim assessment.

© 2026 Faith Ward

This article is published under the following licence:

Terms of Use

See the Faith in RI terms of use on how this work can be used.

Read licence →